When undergoing the process of applying for life insurance, most individuals must have heard of the term “risk class”. This word can be terrifying, especially when you think an examiner would carefully evaluate every risk you have defaulted. In other words, this process is an insurance risk class.

An insurance risk class is a set of people or businesses with comparable characteristics that estimates the risk of underwriting a new policy and premium that can pay coverage. Furthermore, indicating the insurance risk class is a major factor in an insurance provider’s underwriting procedure. Keep reading to gain more knowledge of what the insurance risk class is all about.

How Does Insurance Risk Class Work

Regardless of two individuals not being alike, numerous characters make people to be classified. Moreover, providers must determine if it would be beneficial to underwrite a new policy for a new client or business. However, it’s a bad choice to get a new policy for a significant amount a year if the policyholder ends up filing the same amount for claims.

For instance, a provider might review your age, car’s age, driver’s record, coverage amount, and location, when it comes to car insurance. If you merge these factors, it can produce a profile of a driver, which uses actuaries to understand the driver that fits the profile. Furthermore, the insurance risk class permits providers to estimate the coverage amount that’s necessary with its coverage. The most common use of risk classifications is in life insurance policy underwriting.

Types of Insurance Risk Class

You should be aware that various insurance providers use different standards for rating. Therefore, you may get a preferred select rating from an insurer and a preferred rating from another, depending on the underwriting of both companies. Moreover, smoking or use of nicotine daily can affect your health class and final rates when you apply for a policy. Most providers consider smoking as using chewing tobacco or regular cigarettes with e-cigarettes.

Preferred select rating

If you have a normal height-to-weight ratio, a good health history, and excellent health, you receive a preferred select rating. For instance, no one in your immediate family may have ever experienced an early death from cancer or heart disease. These are the requirements for being eligible for a select rating, though there may be additional non-medical requirements as well. Higher ratings may be assigned to some life insurance companies, like Super Select.

Preferred rating

The preferred rating can also link to an optimal health. However, this rating suggests that you might be more dangerous than someone who would be eligible for a preferred select rating due to several factors. This is because of various factors, depending on the insurer, how the provider distinguishes between a preferred and selected rating.

Non-tobacco rating

For those who use tobacco products sparingly or occasionally, the average applicant can link to a non-tobacco rating, which includes both nonsmokers and . For instance, depending on the insurer, you might be assigned a non-tobacco rating if you smoke cigars occasionally.

Preferred tobacco rating

If you have a preferred tobacco rating, it usually indicates that you would have an ideal rating if you abstained from tobacco use. You will be assigned to the tobacco category despite not having a family history of heart disease, lung cancer, or any other illness related to smoking.

Standard tobacco rating

If you use tobacco and do not fit the preferred rating criteria, but you are still in generally good health, you are likely classified as a standard tobacco user. Even though you have an elevated blood pressure risk, your family’s medical history appears to be favorable.

Your life insurance premiums are influenced by a variety of factors. In addition to your risk rating, they also include the kinds of insurance, the coverage’s duration, and the amount. Your premium rates will take into account all the risks related to smoking, as demonstrated above if you use tobacco products.

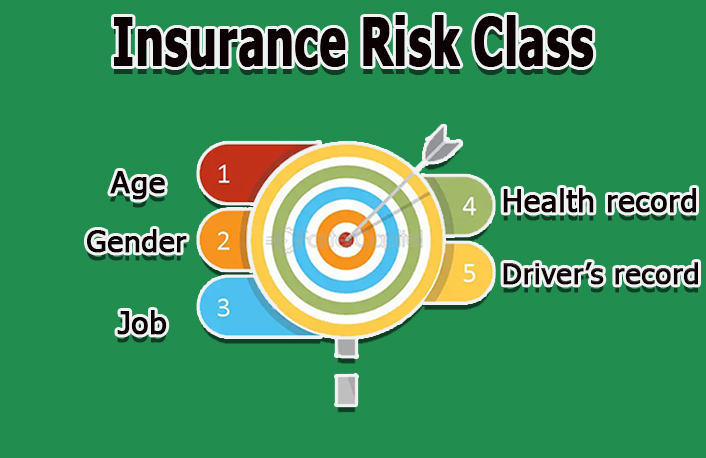

How Insurance Risk Class Is Determined

Before purchasing a life insurance policy, a person must be approved by the company. Underwriters for life insurance oversee this procedure, assessing candidates to determine which risk class to assign and whether they meet eligibility requirements for coverage.

Underwriters look at a lot of different things, such as:

- Gender and age.

- The ratio of height to weight (build).

- General physical well-being, including nervous system, eyesight, hearing, heart, lung, dental, kidney, and kidney function.

- Individual medical background (including prescribed drugs, diagnoses, and treatments from the past and present).

- Medical history of the family, particularly about inherited diseases.

- Lifestyle choices (such as the use of drugs, alcohol, and cigarettes).

- Stability of finances.

- Driving history.

- Dangerous occupations or pastimes.

- Criminal history.

Insurance companies use risk class to group policyholders according to their risk level, which helps them determine the amount to charge in policy premiums. Insurance risk classes are used by providers to reduce their risk.